High-frequency data on the fractional labor market: “ALUR”ing research and policy potentials

High-frequency data on the fractional labor market: “ALUR”ing research and policy potentials

Data is fundamental to economic policy and research. Economists have long used data to inform decisions in both public and private sectors, and have been early adopters of data technology. Advances in data science have enabled new, previously impossible economic models and methods. This creates opportunities for more informative datasets, if accessible.

Data, data everywhere, and not a thought to think

In this age of big data, the persistent and surprising truth is that the demand for data continues to outpace its availability. A primary obstacle lies in the infrequency and lack of granularity within current data sets.

To illustrate this point, consider the FRED repository, which has, since 1991, offered invaluable data concerning inflation, unemployment, GDP, the effective federal funds rate, and various established metrics, in addition to (more recently, perhaps) a comprehensive array of policy and research-relevant variables. Typically, such macroeconomic data has been, and frequently remains, accessible at the conventional quarterly or monthly frequencies.

Financial data provides a stark counter example. Beyond standard asset prices, take for example the Chicago board options exchange's market volatility index (VIX), which is available at the tick-time as well as at higher (e.g. daily) frequencies. The VIX is known by now as the “fear gauge” of international financial markets. In addition to its uses for risk management and investment purposes, the VIX has been heavily and fruitfully used in financial economic research in the past two decades or so.

This said, macro-economic models are still for the most part “taken to the data”, which means “statistically assessed and validated”, with low frequency observations. In this context, the introduction of the Weekly Economic Index (WEI) of US economic activity in 2020 was highly welcomed by the profession. Other welcome indices include the daily economic policy uncertainty (EPU) index introduced in 2016. Another creatively successful use of high frequency data pertains to the quantification of monetary policy surprise (unexpected) shocks: the technical term is “high-frequency identification” which refers to relying on changes in financial asset prices within a tight window (say 30 minutes or so) around key events such as a Federal Open Market Committee announcement. Noteworthy here, with respect to demand for high freq data, is the Atlanta Fed's popular GPDNow.

Yet despite progress, useful data on key economic quantities is surprisingly still lacking. One salient example pertains to the labor market. High frequency or disaggregated data on employment and unemployment remain scarce, with focus on full-time work. Importantly, disaggregated data on part time employment is rarely available, at any frequency for that matter!

Against this backdrop, specific questions endure about the labor market, including the following. What is the relationship between unemployment and job vacancies? What determines the rate at which jobs are filled? What drives transitions in and out of employment? What are the reasons behind involuntary unemployment when open job opportunities are available? Said differently, what prevents job seekers from finding available work? How are wages determined throughout this process? And ultimately, how does all the above relate to economic growth and economic cycles? To address these questions, data is a necessary ingredient!

More broadly, business and government decision makers need reliable information on where the labor market is, where it is headed, what potentials can be untapped and what policies can favourably alter trends.

From the perspective of untapped potential, policymakers and economic scholars need to improve their understanding of involuntary and voluntary part time work, in the context of dynamic economies. To do this, data is a necessary ingredient!

So what is the big deal about data such as the American Labor Utilization Rate (ALUR)?

The prospect of granular data on labor supply and demand, at a frequency that matches say that of the VIX, is by any definition a giant step forward. The daily ALUR index is derived from fine grained and dynamic data on demand (employers) and supply (workers) matches, where demand and supply are not restricted to full time availability. This data also integrates the underlying matching process, as it evolves, for example from a job posting, to views, assignments, scheduling, and eventual cancelations or no-shows.

Three – among many - important features of the above are: (i) its dynamic nature, (ii) its reference to matches, and (iii) its fractional basis.

“Dynamic” specifically means in real-time and over-time, as well as, for example, across different shifts when relevant. The importance of “matches” derives from the fundamental perspective for understanding supply and demand interactions in the labor market, as well as the linkages between labor market movements and economic activity. The premise is that costs, time and other resources (the so-called “frictions”) affect how effectively job seekers and employers look for and find each other, and how wages are bargained in the process. The (joint) dynamic evolutions of unemployment and, conformably, other macroeconomic quantities (GDP, consumption, investment) thus embed the whole “search and matching” process.

Through indices such as ALUR and its underlying real time and fine-grained data, analysts are able to observe and thus measure, monitor, and represent the search and matching process in question. Since this process is integrated into the measurement, tracking and description of economic activity, growth and cycles, the benefits of data such as ALUR have broad transformative potential.

Last but not least, ALUR provides detailed information on the fractional labor market. Fractional work refers to part-time or project-focused activities without the commitment of a full-time position nor of a single employer. Fractional work is offered and pursued at all skill, specialization, talent and expertise levels. Whether voluntary or involuntary, businesses and economic policy makers can no longer ignore rising and fractional demand and supply trends. Despite burgeoning research through the cooperation of a few academists and labor market analytics companies, what economists have learned so far hardly scratched the surface of what can be learned.

Yet fractional work is a real and evident reality. The Bureau of Labor Statistics indicates a slight, yet significant, dip in the average weekly hours per U.S. worker, falling from 38.8 hours in 2021 to a projected 38.2 hours per week in 2025. While 36 minutes may seem negligible on an individual basis, when multiplied across a labor force of approximately 170 million, this represents a staggering loss of productivity equivalent to 2.55 million additional full-time (40 hours per week) workers. This is precisely what a fractional workforce perspective can help reclaim.

To be specific, consider the WorkWhile platform: powered by AI, WorkWhile connects qualified individuals with opportunities that leverage their skills and fit their desired flexibility. The net effect is more hours worked, which on the aggregate will contribute meaningfully to a more productive economy.

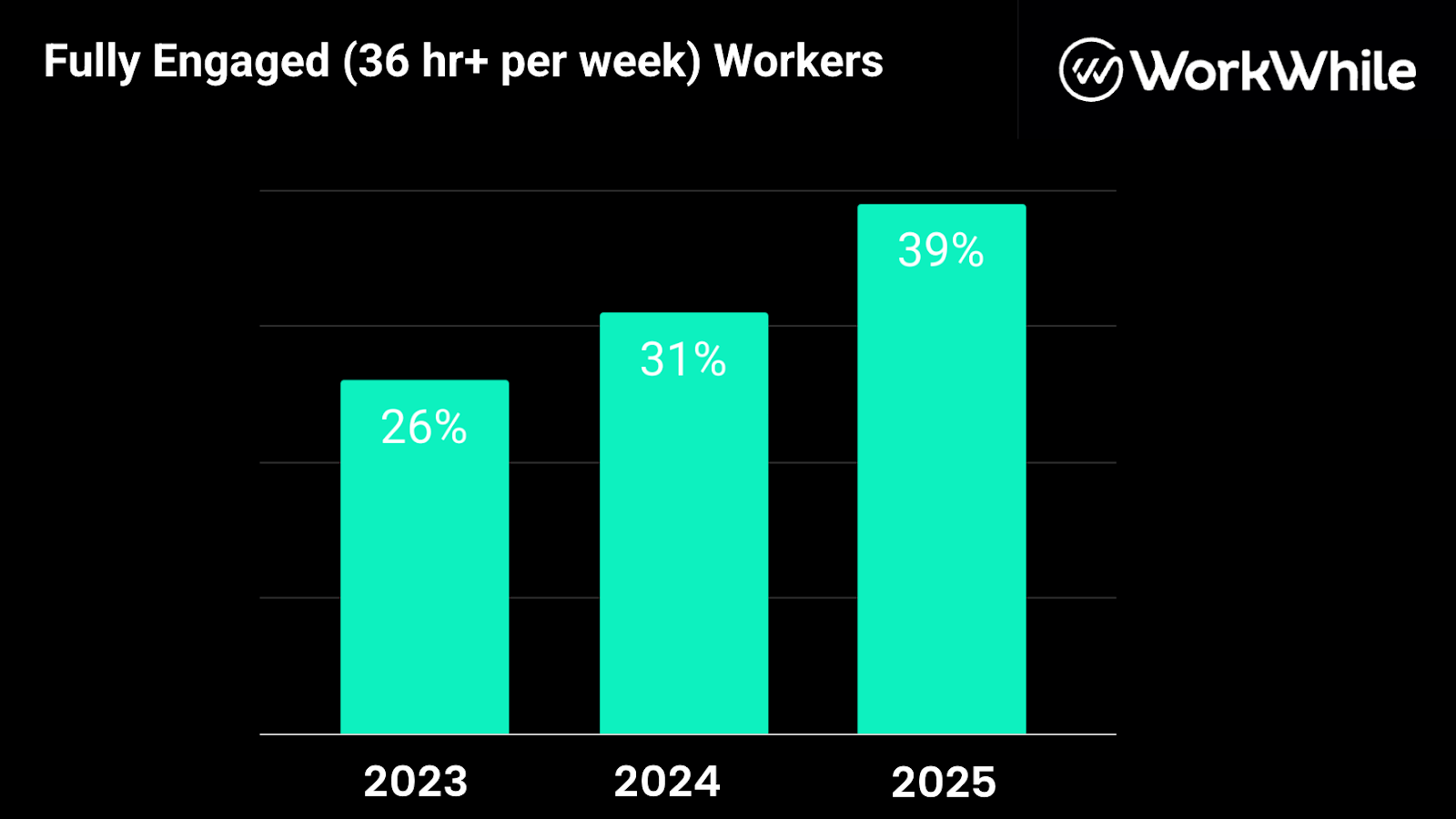

Turning to the data, the chart below illustrates such impacts focusing on the WorkWhile ecosystem: the percentage of WorkWhile's workforce achieving fully engaged status (36 hours or more per week) is on a visibly upward trajectory, 26% in 2023 to 31% in 2024 and to 39% in 2025.

In addition, WorkWhile’s newly released American Labor Utilization Rate (ALUR) has shown that worker retention on the platform has consistently been above 96% and has recently reached over 99%, even as the commitment for continued employment is not granted.

Fractional work is “work”

Beyond filling part-time roles, these figures suggest that job seekers and job suppliers can effectively piece together multiple engagements to achieve or even exceed traditional full-time hours. Fractional work can thus provide a stable and sustaining income stream, for voluntary or involuntary part-time workers. By effectively mobilizing this talent pool, businesses can boost productivity and scale job offerings up or down, without the rigidities associated with traditional hiring. Fractional work thus does not mean less work at the individual and firm level, and thus at the aggregate level.

In conclusion, the fractional workforce is no longer a fringe concept; it is a critical component of a dynamic economy. There is no doubt that data such as the ALUR index and underlying fine grained high frequency observations will shift the landscape for economic policy and research.